Understanding and playing the credit card game

Most people worldwide don’t use credit cards to pay; amongst those who do most people don’t use them intentionally; they’re just a delayed debit card with maybe a few perks thrown in. The final category is the intentional card users who are doing it for primarily two reasons: Status, Savings. The Apex predator of the credit card game is the luxury/lifestyle card when you pay a huge annual fee but get perks, subsidies, to make up for the fee.

Should people bother with credit cards? Or avoid them like the plaugue? Let’s explore.

What credit card companies want you to think

Let’s look at some credit card branding attempts.

Source: Chase’s New Sapphire Reserve Credit Card

Source: Chase’s New Sapphire Reserve Credit Card

Source: 2025 Press Kit: Platinum Consumer and Platinum Business Card Updates

Credit card branding is all feel good and “unlock a new world of possibilities”. It’s all luxury, travel, restaurants, etc. Come get these cards be a part of the jet setting elite. Credit cards are speaking to you as a consumer and telling you that nothing is beyond your reach. Look at a beautiful model holding our beautiful card. You too will feel beautiful when you hold our credit card.

How credit card companies actually make money

Credit card companies have three main sources of income:

- Processing fees:

- 4% of income

- Typically 2-4% and not paid by the consumer. These are paid by the merchant/seller and baked into the cost of goods.

- Interest:

- 80% of income

- Paid by the consumer when they don’t pay their balance in full. Typically 20% or so, always much higher than the interest charges on a personal loan.

- Fees: Foreign transaction fee, cash redemption, etc.

- 15%-16% of income

- Paid by consumer often unknowingly

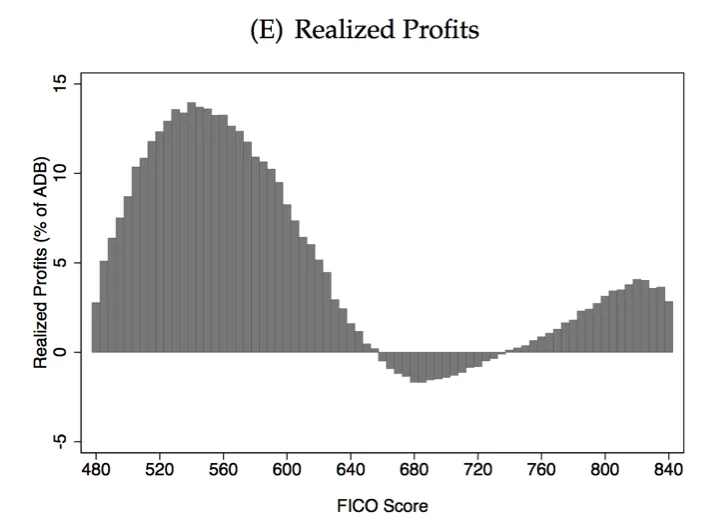

Source: The Fed - Credit Card Profitability

They make money differently from different people; here is a graph of profits by credit score. The credit card companies are making the most money from low score aka poor people, losing money on middle score people and earning some money on the richest people.

Source: Regulating Consumer Financial Products: Evidence from Credit Cards

Source: Regulating Consumer Financial Products: Evidence from Credit Cards

How does this happen? Amongst the low score/poorer people, credit cards companies are making tons of money from interest charges and fees. It’s possible to imagine the poorer people running into financial distress more often and relying on credit cards to get by. While ideally, they should use personal loans with lower interest rates, it is way more convenient to just swipe your card. With the low score people, there isn’t much payment volume to go around. On contrary, at the upper end, the high score/richer people can spend more so companies earn more from the higher transaction volume. The interesting part is the middle score range, the person isn’t spending enough to earn the company a lot in payment processing fees; neither are they borrowing credit and paying interest; this results in a loss for the company!

So, while companies market themselves as high status lifestyle tools of the jet setting elites, they actually make the most money from poor people paying interest!

Credit card traps

Credit card companies are counting on a couple of things to make money.

- Financial trouble

- You will get into financial trouble and make the mistake of leaning on your credit card; when you should actually take out a personal loan

- Overspending

- You will get incepted with the idea that you deserve to buy something. You will buy expensive things you can’t afford from your own savings/earnings; and fork out tons of interest.

- Mistakes

- You will forget to pay your bill, incurring interest despite not officially needing credit

- You will forget to redeem your perks thereby losing your chance to redeem the fees you paid upfront

- You will not notice when your credit cards points are devalued, restricted, expired, etc. or some other restrictions are placed that make it more challenging to get the most/promised value from your card

- You will use your card at a foreign merchant and incur hefty foreign transaction fees.

Credit card companies are counting on your misfortune, your profligacy, and your inattention to make money

Playing the game wisely

With that said; credit card companies do throw many perks your way, be it hefty sign-up bonuses, high cash back rates, crazy offers, etc.

General principles to succeed here are:

- Do not manufacture spend: Ideally the rewards or perk fit into your existing lifestyle. The moment you have to go out of your way to purchase random shit to clawback your high card fees, you are being a sucker.

- Split your spend into segments; use the most rewarding card for each category.

- Start with your largest category and then try to get the highest cashback there

- Consider a lower cashback/rewards rate temporarily, if you are getting a sign-up bonus or other offer.

- Go back to your best credit card once the offer period expires or offer is complete. This is called “churning” and companies obviously hate it. A risk with churning is that you can get banned by credit card companies!

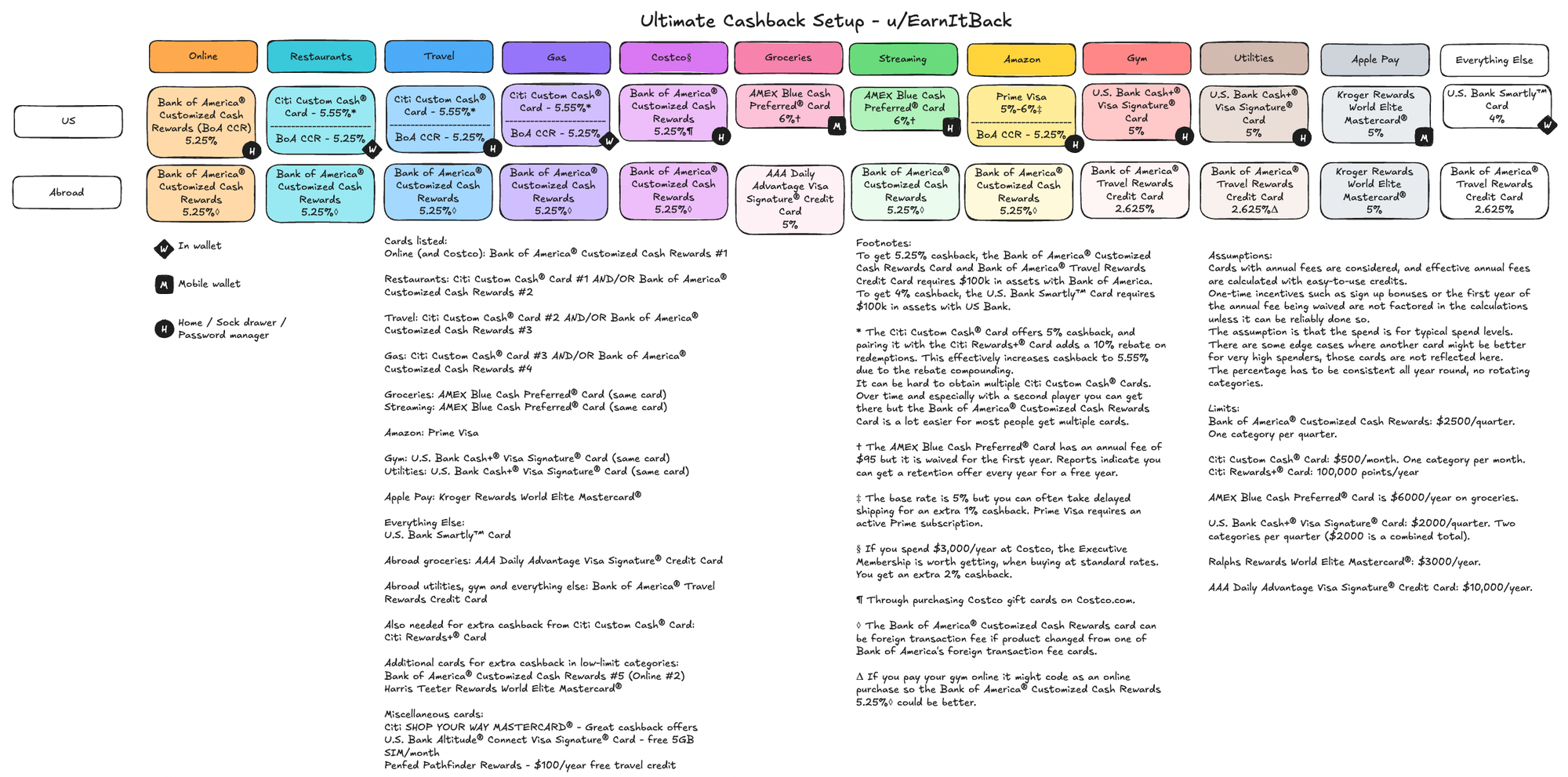

The logical endgame of this spend segmentation is this: 8072ab0f86.jpg (2000×991)

{kind=link}

A multitude of credit cards for each category, spending carefully using the card of each category and maximizing your earnings.

Objections to being in the credit card game

Cognitive objections

I am a parent living far away from my family with a demanding household workload. 2 years ago I did have the time to create spreadsheets and track spends, etc. Not anymore. I don’t think it is worth it. A few more hours of exercise; a new jobs with better pay can impact me much more than cashback. Now this is my case of a super diligent finance MBA guy!

My wife is not a credit card maximizer; she’s the average credit card user. A person likely to miss the fine print and lose because of devaluations. This is what happened with her Capital One Venture X card (which she has because she loves travelling)

The $300 travel credit on the Capital One Venture X card is changing from being a statement credit to becoming a coupon you apply to your purchase at checkout on the Capital One booking portal. This is a slight devaluation for a few reasons:

- If you purchase a refundable ticket and cancel, you’ll get back the $300 coupon for future use. BUT you won’t be able to keep the $300 statement credit, as was previously the case. (It should still be possible to bank the credit with an airline who offers such a cancellation policy.)

- We will no longer earn 5/10x on the purchase for that $300 charge since the cost is simply reduced as a coupon.

- The $300 in spend will no longer count toward your minimum spend requirement

Source: Capital One Venture X Changes $300 Travel Statement Credit Into $300 Coupon - Doctor Of Credit

Imagine being a new mother worried about your child’s growth and then having to keep track of shit like this.

Overall, credit cards and rewards need constant tracking which becomes a part time job; very often not worth it.

Moral objections

Credit card perks are coming from an unfair advantage given to credit card users. I believe that good should be priced equally for all. However, due to one subtle policy; credit card users effectively get a discount.

A merchant thinks “Hey I will sell this for $100”, most merchants start with a baseline of cash or debit cards, and prices things at $102 figuring in payment fees. However, costs are not the same for all payment methods. Cash is free; Amex cards go as high as 4%. Now logically, if you want to pay with an Amex, ther merchant still wants to get paid $100 for the item. They should charge you a $4 processing fee. But in many places, the law forbids this! The merchant is obligated to charge $100 regardless of payment method and eat the cost of processing an Amex card. Hence you see many merchants not bothering with Amex at all! Everyone always has an alternate card anyway; so they don’t really lose business. Additionally this hurts small businesses the most. Big businesses can negotiate these rates because of the huge payment volumes they drive; small businesses are left in the lurch.

The equal price rule is a free market distortion; and effectively serves as a tax on the business and sneaky redistribution of money from the poor to the rich.

My public policy stance is that

- Payments are so critical to the economy that it should be a public good. This has been achieved in countries like India, China and Brazil.

- Private payment methods should exist alongside public payment methods run at zero processing fee with taxpayer funding and/or minimal interchange.

- Merchants should be allowed price discrimination based on payment method to keep their margins intact

- Alternatively; you can cap processing fees (like Europe did).

- Price discrimination should be implemented automatically. if you get a bill of $100; that should be what the merchant wants. If you use a debit card, you get a discount, regular cards, you pay the bill; if you use a luxury/high interchange card; you pay extra.

Spiritual objection

At some point, the goal is not making more money but living a better life.

Financial counter-objection

If your net worth is below $100K; being smart with credit points and sign-up bonuses can genuinely serve as an income boost of a few hundred to at max a few thousand dollars. But once you’re over the $500K net worth threshold or above the $200K income threshold, you’re betting off investing your money smartly or getting a new job or …

My current strategy

After having played with annual fee cards with Amex platinum and gold, I felt the mental effort of tracking my rewards and redemptions wasn’t worth it. I did score loads of point and get free flights; but I felt that it was becoming a part time job for me. My time and attention were better spent elsewhere. As I’ve become a parent and have more responsibilities and life duties; I have absolutely no room for this. I’ve switched to cashback cards. I have the Robinhood card for 3% cashback everywhere and AAA Advantage Daily card for 5% on groceries. That’s it.

I did consider the BILT credit card as rent is my highest expenditure but the company has added multiple conditions to make sure you don’t just pay rent with the card and throw it in the sock drawer. I was not in the mood for that song and dance, so decided not to use it.

Conclusion

Credit cards should be handled with care. While marekted as lifestyle enablers, they make most money from financial mistakes. They offer money when you need and can potentially earn you some as well. However, they encourage lifestyle creep and overconsumption; and are also overall a distraction to be careful about.